Should the Government Relent?

Property experts are calling for the government to walk back a ban on self-managed super fund loans for residential property, amid claims the true impact on new housing supply may be bigger than modelling suggests.

The forthcoming ban is a blanket one, encompassing both new and existing homes – this is at odds with the negative gearing changes announced in May’s federal budget where new homes are exempt.

Industry figures hope the impending rule change could be partially walked back, similar to how the minimum tax rates placed on trusts were later amended to exclude testamentary trusts. This captured inheritances, left via a will, and critics called it a ‘death tax’.

Like the so-called ‘death tax’, experts are saying the residential loan ban for SMSFs could have far-reaching and unintended consequences, chiefly for the pipeline of new homes.

Many industry experts believe that SMSF loan ban would hamper the government’s densification efforts and the types of homes it is trying to build under the National Housing Accord.

SMSF buyers are likely to appear in specific types of stock: new apartments, townhouses, house-and-land packages and investor-oriented dwellings at lower price points. These are also the projects where pre-sales can be hardest to achieve when investor demand is weak.

Typically, for a new development to draw down on finance and start construction, around 60% of units in a complex need to be pre-committed, with SMSF buyers commonly in the pool of those buying off the plan.

This means if one off-the-plan unit backed by an SMSF falls away, it could have a domino effect on the viability of the whole project.

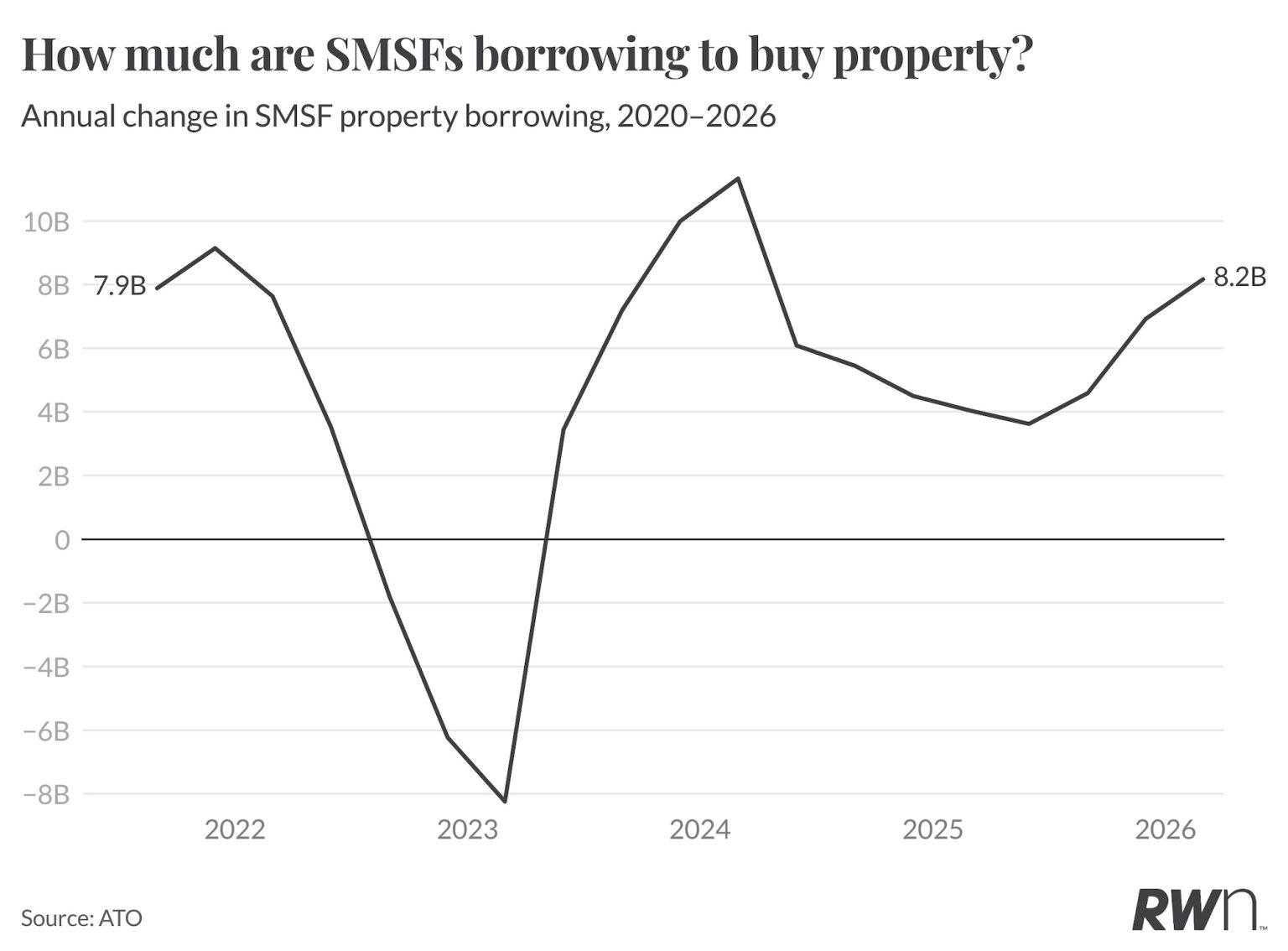

The government says the rule change is small in scope, with fewer than 4,000 SMSF loans written per year.

Developers estimate around 30% of off-the-plan purchases are backed by SMSFs. If the conservative 4,000 figure is correct then upwards of 13,000 units are at risk, though it’s unclear on the split between loans for new versus existing dwellings, or the proportion of off-the-plan purchasers that are leveraged.

Many in the sector say 4,000 is likely a significant undershot of the true figure.

Several SMSF loan providers opened their ledgers up to the Financial Review last week, revealing a much higher number written over the past 12 months.

REA Group economist Luc Redman also said the ban could have a surprise effect where some SMSFs with enough cash look for established properties, rather than take a punt on higher-risk off-the-plan builds as they are using more of their own capital.

“These changes won’t directly impact SMSFs’ desire to gain exposure to residential property as an asset class, but will most likely mean that exposure is skewed towards established dwellings rather than higher-density developments, exactly where supply is required.”